Instead of this week’s Founder Friday post, I have decided to share the ‘Q4 & 2022 Year-End’ update that I sent out earlier this week to more than 100 SuperAngel.Fund LPs. I have removed any private information for confidentiality purposes. Hope you enjoy reading it and welcome any thoughts, questions or feedback (ben@superangel.vc).

Dear Partners,

I am pleased to share the Q4 & 2022 Year-End Update for SuperAngel.Fund.

Before going into a review of our portfolio and activity, I would like to address some of the larger themes playing out in the market, as it is a topic that is likely on the forefront of everyone’s minds.

General Market Conditions

While the public and late-stage private markets continue to fluctuate, early stage investing, particularly at the pre-seed and seed levels, remains somewhat insulated. This is because an early stage investment today, if successful, is not expected to reach maturity or an eventual liquidity event for another 5-10 years, when we are likely to be in an entirely different market environment.

According to Cooley, which handles more venture financings than any other law firm in the US, the amount of capital invested, and number of financings, have decreased substantially in the last quarter, with the most pronounced impact affecting later-stage deals (Series C and beyond). Additionally, the amount raised during Q3 2022 as compared to Q4 2021 dropped by 50% or more for Series A or later deals, yet decreased by only 9% for seed stage deals. Per Cooley, “The more significant drops in later-stage deals compared to early-stage deals is expected, given longer time horizons to exits in early-stage deals, leading to more stability for investors.”

Valuations also declined across the board, with the largest decrease occurring in later-stage deals too, and only a slight decrease at the seed stage, going from a median pre-money valuation of $18.6m in June 2022 to $17.6m in September 2022. Per Cooley, “The average pre-money valuation for seed deals has remained relatively consistent since late 2021.” After all, there is somewhat of a fixed floor for startup valuations that account for a simultaneous attractive ownership level in the present while also allowing for proper flexibility for future financing needs.

That said, these figures do not yet incorporate deals closed in Q4 2022, which, I believe will show a much more substantial decline in valuations for pre-seed and seed rounds than the preceding quarters of the year. If my inclination is correct, the next few years may be some of the best to invest in early stage companies.

Impact For Our Fund

I believe the trends above will continue over the next 12-24 months. We are likely to see further downward pressure on valuations, particularly for first time or otherwise overlooked founders, within our sectors of focus. Our own data over the past two quarters has also shown new deals priced more reasonably, both for follow-on investments in our top performers, and for new companies as well.

While there is historic amounts of venture capital dollars on the sidelines, much of it waiting for the market to feel more “stable”, we continue to invest, seeking founders and opportunities that go against the herd. As Warren Buffett famously said: “Be fearful when others are greedy, and be greedy when others are fearful.”

Per a Wall Street Journal article from November 2, 2022:

“Venture has outperformed other asset classes in prior down cycles. About 75% of venture-capital funds raised from 2007 to 2016 beat the Russell 2000 during that time, and roughly 60% beat the S&P 500, according to a 2021 research paper published in the Harvard Business Review. According to research from the University of Miami, venture-capital returns during the dot-com crash and the 2007-09 recession averaged a 16% gain, while the S&P 500 lost 12% and the Nasdaq declined 18%.”

Below is a recent comment by Jason Lemkin, one of the most successful and well respected early stage VCs, that I felt was worth sharing:

Here is another well-researched post from industry thought-leader Evan Armstrong titled “It is Always Time to Build” that I encourage reading (h/t Howard Lindzon):

“While there is some merit to the idea that when interest rates are lower, risky ideas are funded because returns are more challenging to find, it misses how great companies begin. If you’ve read the histories of Gates, Jobs, Ford, or Edison, they didn’t worry about federal interest rates when they started their companies. Technology companies came to be because scientific advancement met charismatic founders and risky happy financiers…companies are built with science, ingenuity, and sheer hustle to find and capitalize on a market opportunity. Regardless of the interest rate, it is always time to build.”

Aside from more attractive entry points, a larger number of higher quality deals are coming our way because of the reputation, credibility and network we have established as a leading fund at the pre-seed/seed stage. We are also benefiting from deals moving a bit slower, providing more time to diligence and build a deeper relationship with founding teams. The companies we are investing in today are being shaped during more disciplined times, creating a higher degree of resilience more commonly held by the most successful, enduring companies.

Entry Valuation Analysis

Fund Performance

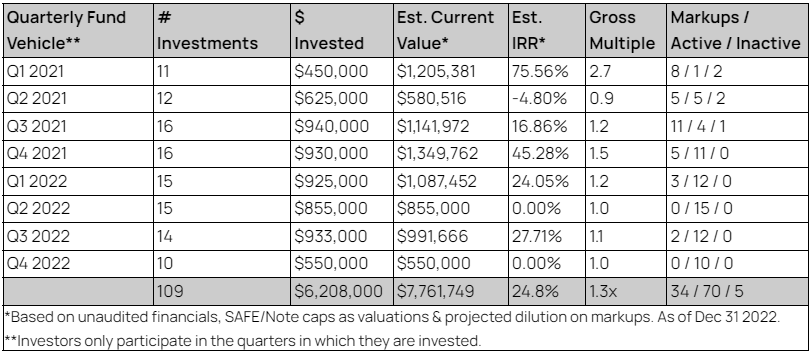

Since the fund started on January 1, 2021, we have invested $6.2m into 86 companies across 109 investments. I estimate the current net asset value at $7.76m, representing a 25% unrealized IRR and 1.3x gross multiple.

Out of 109 investments, 34 have raised additional capital at a higher implied valuation than we invested at, 70 are active yet to close a subsequent financing and 5 are inactive (or projected as such). The real value, however, will be determined in the future once our companies have time to mature and reach their potential. Of course, my job is to realize gains and turn them into distribution events for investors. Below is a summary of our performance:

> Click here to view a detailed performance tracker [Fund only]

> Click here to view a detailed performance tracker [Angel, SPVs & Fund]

As layoff announcements consume much of the headlines, we are still seeing strong updates from many of our large basket of portfolio companies. Some are using these times as an opportunity to lap emerging competitors or industry incumbents, leaning into the downturn by hiring more experienced and capable talent than was previously available to them. Top performers continue to get funded, with a few notable examples below that closed a follow-on markup round during 2022:

EcoCart: Sustainability platform for brands

Cadence: Personal care, sustainable travel system

Bounty: Unlocking the power of influencer marketing

Rubik: Investment platform for Single Family Rentals

Intelligems: Revenue optimization platform

Windmill: Eco-friendly, clean air products

EIGHT: A new iconic American beer brand

Merri: Event planning tools & marketplace

EarlyDay: Talent marketplace for early childhood education

Home From College: Career development platform for Gen Z

Motion: Creative analytics platform for growth teams

Confetti: Unforgettable team building experiences

Pack: Modern storefront for headless commerce

Arber: Modern lawn, garden & plant care brand

Q4 2022 Update

During the fourth quarter, we made 10 investments with a median check size of $50k and post-money valuation of $15m. Our investments were spread across Consumer (3), eCommerce SaaS (4), and PropTech / Future of Work (3).

> Read the Q4 2022 Recap here 📝

Packsmith: Distributed fulfillment for brands

Flexbase: Finance super-app for small businesses

Krava: Reimagining the future of sustainable spaces

Two Boxes: eCommerce returns processing platform

Popsmith: Reimagining the popcorn experience

Candidate.fyi: The missing candidate experience layer

Arber: Modern lawn, garden & plant care brand

Otis: Modern pet care platform

Stealth / TBA

Stealth / TBA

There are exceptional entrepreneurs everywhere building exceptional companies, and we spend most of our time trying to find them, and buy a ticket on their rocket ship. I maintain deep conviction in our fund’s strategy, and believe the market turbulence will continue to work in our favor as we sit on a healthy cash position, ready to take advantage of opportunities. To rearticulate our approach:

Invest as close to the first check as possible

Focus on the categories we know best

Leverage our massive network on behalf of portfolio companies

Provide operational, sales & team support to deliver unfair competitive advantage

Champion our companies religiously to drive incremental exposure, customers, and business opportunities

Position ourselves as each founder's favorite and most helpful investor

Many of these attributes result in higher quality and larger quantities of deal flow, one of the most pivotal aspects of any type of investment firm.

We also believe that the earlier the stage that one invests (and we invest very early), the more diversification is needed to weather the zeros and optimize the chances of hitting home runs. As you know, it is a tremendous amount of work to source, diligence, and assess these businesses. This is work I love, and what I feel is needed to deliver above market returns over an extended period of time.

As always, the fund has a strong pipeline for new investments and will continue to monitor follow-on opportunities into existing portfolio companies that show breakout success/growth metrics. If you come across impressive founders looking to raise capital within our areas of focus, I appreciate you sharing those opportunities with me (ben@superangel.vc).

Thank you for your ongoing support and confidence.

Sincerely,

Ben Zises

SuperAngel.Fund

PS - In case you missed it, our fund was recently featured by Mintz Levin in their newsletter series: “MintzTech Connect Industry News: Spotlight on Ben Zises and SuperAngel.Fund,” written by Daniel I. DeWolf, Chair, Technology Practice, Co-chair, Venture Capital & Emerging Companies Practice.

SuperAngel.Fund is an early stage fund that invests in Consumer (CPG, eCommerce SaaS), PropTech & Future of Work.