SuperAngel.Fund Ranks in the Top 1% 🥇

SuperAngel.Fund is an early-stage venture capital fund investing in Consumer, PropTech & Future of Work.

Dear Friends,

One year ago, I launched SuperAngel.Fund II.

Since then, 100+ LPs have committed to invest alongside me, and we’ve made 60 investments across 45 companies, with 20 already marked up.

While we are still early in the journey, I’ve never been more confident in the quality of our portfolio and the long-term potential of the companies we’ve backed.

Based on AngelList’s proprietary performance data, SuperAngel.Fund ranks in the top 1% of GPs on markups over baseline, which AngelList believes is one of the strongest leading indicators of future venture fund performance.

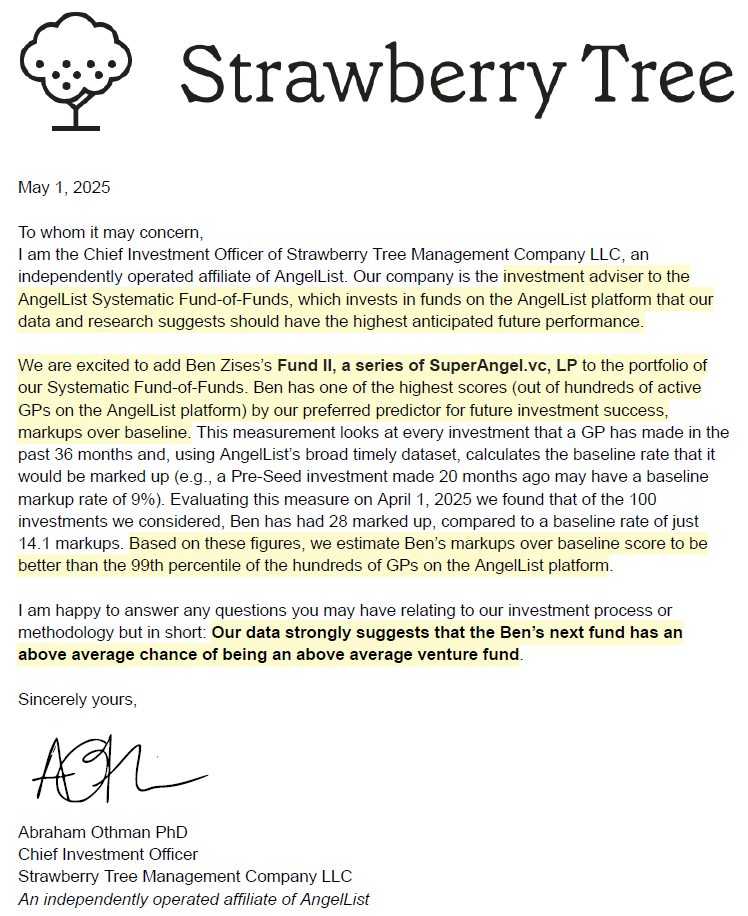

Last year, I received an unsolicited email from Abe Othman, Chief Investment Officer of Strawberry Tree Management, investment adviser to the AngelList Systematic Fund-of-Funds.

Based on their internal data and underwriting, the AngelList Systematic Fund-of-Funds invested $800,000 into SuperAngel.Fund II.

The Fund-of-Funds is backed by Sequoia Capital, Squarepoint (a $100B+ quantitative asset manager), Naval Ravikant, and others.

While no outcome is guaranteed, I view this as meaningful third-party validation of both our strategy and early execution.

Below is a copy of their signed commitment letter: ⬇️

Fund II Portfolio

Investments across Consumer, PropTech & Future of Work

How we invest

Fund II is designed to make approximately 100 investments across 60 companies over a four-year deployment period.

We invest as early as possible — typically Pre-Seed through Series A — where ownership can be established at attractive prices.

From there, we stay close to founders and selectively increase ownership as breakout growth and supporting data emerge.

The strategy is intentionally simple:

Early entry valuations → disciplined pricing below market averages

Broad diversification → maximize exposure to breakout outcomes

Access advantage → a growing founder and LP network continues to improve deal quality and access

In early-stage investing, access and diversification matter. Research from Carta and AngelList continues to reinforce that broad portfolios meaningfully improve the probability of capturing outlier returns.

A favorable vintage for early-stage investing

Recent changes to Qualified Small Business Stock (QSBS) rules further improved the after-tax profile of venture investing — including higher exclusion caps, shorter holding period benefits, and expanded eligibility.

Combined with disciplined entry pricing, broad diversification, and improved after-tax treatment, I believe this creates an attractive environment for long-term early-stage investing.

Venture investing can often feel like a black box. I believe LPs deserve more transparency, access, and communication.

Beyond returns, I strive to build an investing experience that is unusually transparent, accessible, and communicative — with regular portfolio updates, direct access, and a front-row seat to the journey of building enduring companies.

Fund II is scheduled to hold a final close at the end of 2026, after which we do not expect to accept additional LP commitments.

If you’d like to learn more, simply reply to this email and I’ll send over additional materials, portfolio updates, and access to our investor portal.

Why am I receiving this email?

You’re receiving this because you’re part of the SuperAngel Network — a friend, founder, co-investor, or connection who has expressed interest in receiving updates.

If this isn’t relevant, you can unsubscribe below.

this is very consistent with what Carta's research has shown for years. index-style angel investing outperforms concentrated bets at the pre-seed stage. the QSBS expansion mentioned in the post is real and material for any US founder thinking about cap-table structure now